Really, it’s everyone’s issue: The health care crisis in this country affects all of us, even those fortunate enough to have coverage. But when it comes to health care and dealing with insurance companies, there are special concerns for women, especially if they are buying insurance through the individual market. Some of those concerns vary by state, making them all the more confusing, and unfortunately, a lot of women are unaware of these issues until they run into difficulties. Federal laws provide certain protections for women who receive insurance through their employers, but women purchasing insurance through the individual market face unique problems. They face institutionalized sexism in the form of higher costs, shoddy plans riddled through with gender-based exceptions, and denial of coverage based on a “preexisting condition” that may surprise some of you.

According to American Progress,

Women are more likely to have to seek coverage on the individual market than men as they are less likely to qualify for employer-sponsored coverage. However, being a woman means paying more for health insurance. Pregnancy has long been a reason insurance companies use to charge women higher rates for health insurance, even though many individual insurance policies don’t even cover maternity benefits.

In 2008, the National Women’s Law Center released a report entitled Nowhere to Turn: How the Individual Health Insurance Market Fails Women. Their findings indicate that women seeking insurance through the individual market face tremendous challenges.

Different rules apply to insurance offered by employers versus insurance sold directly to individuals. For example, important state and federal anti-discrimination protections apply to employer-provided health insurance-but not to health insurance sold in the individual market. Under Title VII of the Civil Rights Act of 1964, employers with 15 or more employees are prohibited from charging employees different premiums for health insurance based on gender or other factors. Almost every state has a law against sex discrimination in employment along the same lines as Title VII. The majority of these state laws have an employee threshold that is lower than Title VII, meaning that the state prohibition on sex discrimination in employment could apply to employers that are too small to be covered by Title VII. Courts and state officials have applied these laws to employer’s health benefit plans. Thus, employers unlawfully discriminate under state and federal law if they charge female employees more than male employees for the same health coverage.

Similarly, state and federal anti-discrimination protections ensure that most employer-sponsored insurance covers maternity expenses. The Pregnancy Discrimination Act of 1978 amended Title VII to specify that discrimination on the basis of pregnancy, childbirth, or related medical conditions constitutes unlawful sex discrimination under Title VII. Under the Pregnancy Discrimination Act, any health insurance provided by an employer with 15 or more employees must cover pregnancy on the same basis as other medical conditions. Correspondingly, the fair employment laws in almost all states consider discrimination based on pregnancy to be sex discrimination, and the majority of these laws apply to employers that are too small to be covered by Title VII. As a result of state and federal anti-discrimination protections, most women with job-based health insurance receive maternity benefits.

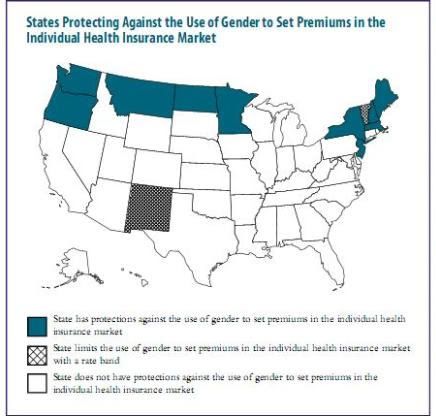

Insurance on the individual market, however, is generally a state issue, and regulations vary greatly by state. A process known as “gender rating” allows insurance companies in many (most) states to charge women higher rates for coverage than men.

Currently, insurance regulation is mainly a state-by-state patchwork. And in most states, insurers are allowed to charge women in their childbearing years more than they charge men of the same age.

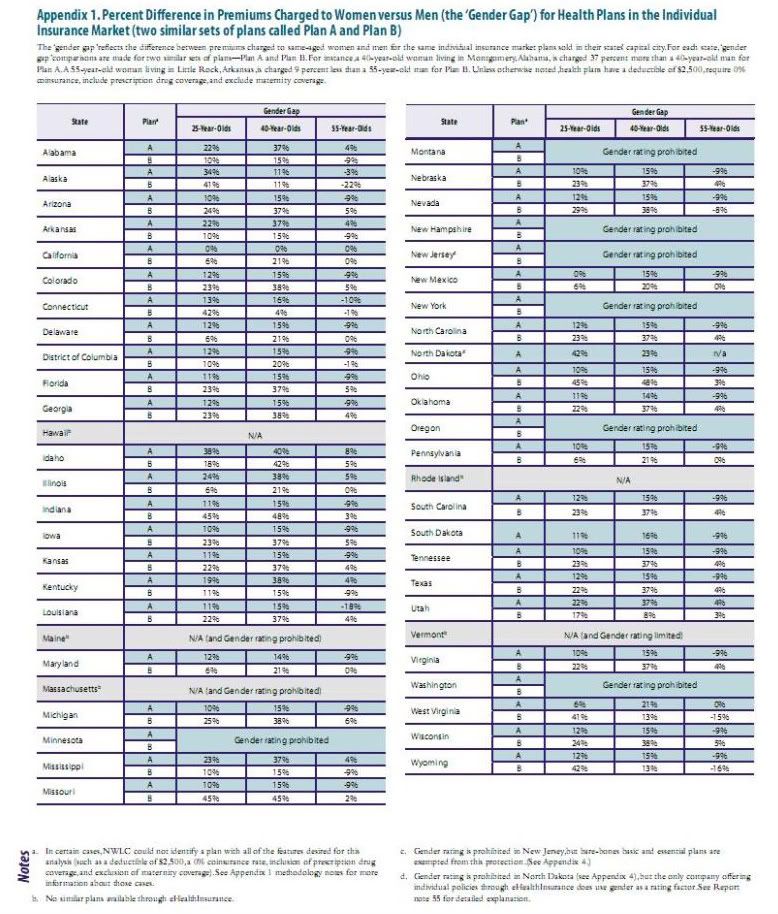

According to a 2008 study by the National Women’s Law Center, companies that practice so-called gender rating charge a 25-year-old woman up to 48 percent more than they charge a 25-year-old man, though by the time a woman is 55, she is likely to pay up to 22 percent less than a man.

Representatives of the insurance industry argue that gender rating is actuarially justified-or that it reflects actual differences in the cost of providing health insurance to women versus men; they contend that premiums are higher because women, on average, have higher hospital, physicians’ and other health care costs than men.

And why do we have higher costs? Well, in part, it’s because we actually use the services we pay for.

In general, insurers say, they charge women more than men of the same age because claims experience shows that women use more health-care services. They are more likely to visit doctors, to get regular checkups, to take prescription medications and to have certain chronic illnesses.

Yes, women are penalized even for taking preventative measures and getting regular checkups (you know, like people say you’re supposed to do). One might expect, at the very least, that those higher cost would cover maternity care — but one would be wrong.

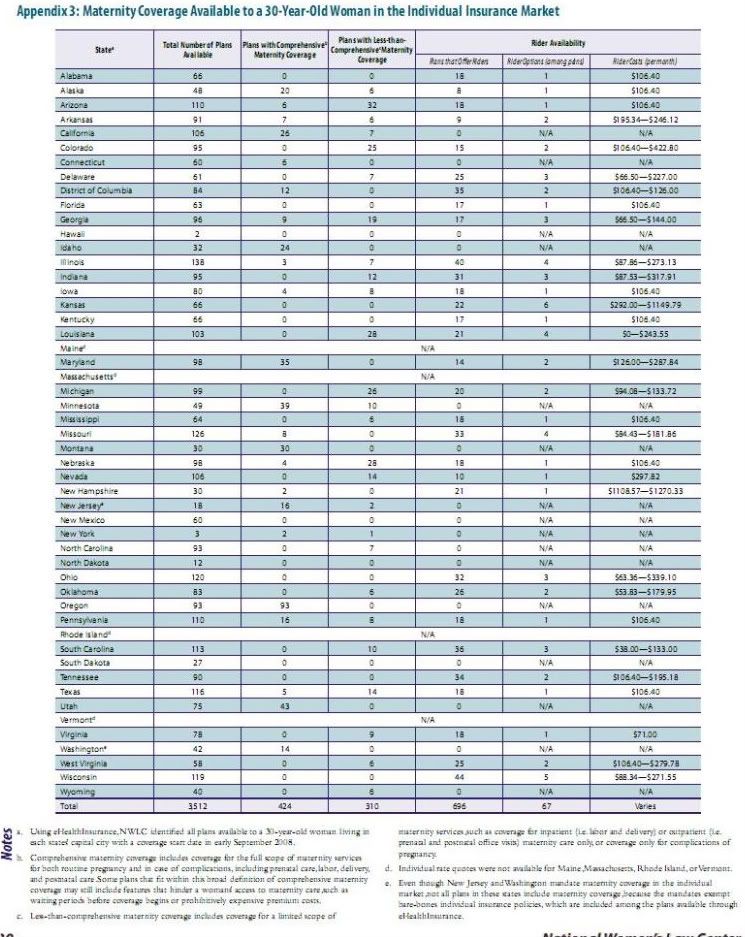

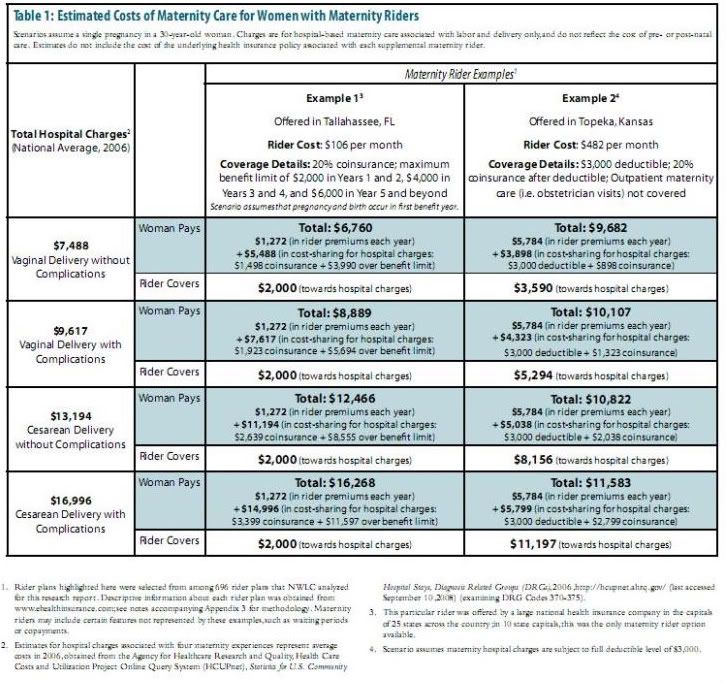

Individual market insurers may consider pregnancy as grounds for denying a woman’s application, or as a “pre-existing condition” for which coverage can be excluded. An uninsured woman who wants to purchase individual market coverage after she is already pregnant will probably not receive any offers of maternity coverage at all-in most states, individual market insurers are allowed to deny coverage altogether to a pregnant applicant. Even if they are required to issue a policy, insurers are generally allowed to consider the pregnancy as a “pre-existing condition” and will exclude coverage for maternity services. A woman’s age has an impact on whether maternity benefits are available in a health insurance policy, and at what cost-a 25-year-old woman is likely to have significantly more options, at a more affordable price, for maternity benefits than her 35-year-old counterpart. Past maternity care experiences can also have an impact on the ability to obtain health insurance; women who have given birth by C-section may encounter additional barriers when trying to purchase coverage through the individual market. An insurance company may charge a woman who underwent a previous C-section a higher premium or impose an exclusionary period during which it refuses to cover another C-section.

The vast majority of individual market health insurance policies that NWLC found do not cover maternity care at all. Even if a woman is not currently pregnant, it is unlikely that an insurer will provide or even offer maternity benefits as part of her regular insurance policy.

[. . .]

In addition to their prohibitive cost, maternity benefit riders may involve a waiting period (one or two years, for example) before the coverage even takes effect

and the actual benefits provided through riders are very often limited in scope.

Congressional Democrats are trying to put an end to this sort of sex-based discrimination, and the Times points out that, “The health care bills in Congress would require maternity coverage and would generally bar insurance companies from charging women, even in their childbearing years, more than men.” I wonder if the Republican women we saw frothing at the mouth during the 9/12 protests Saturday have any idea how many protections that evil, fascist, reincarnation of Hitler president of ours and his allies in Congress are trying to afford women. My guess is no. Then again, there’s a good chance that would only harden their stance against him. After all, conservatives — even conservative women — don’t have a whole helluva lot of use for us ladies. Hell, Coulter doesn’t even think we should be allowed to vote.

But then some insurance companies have another, subtler way of discriminating against women. Apparently in DC, Arkansas, Idaho, Mississippi, North Carolina, North Dakota, Oklahoma, South Carolina, South Dakota, and Wyoming, domestic violence is a preexisting condition. Now, I am not saying that domestic violence is exclusively a women’s issue, but the Department of Justice estimates that over 80 percent of spouse abuse victims and dating parter abuse victims are female. Thus, a policy of denying coverage to victims of domestic abuse disproportionately affects women. I find it mind boggling that nine states and the District of Columbia still allow such practices.

The need for health care reform has never been more urgent. As the economy struggles, more and more unemployed women (and men) are being forced to seek insurance through the individual market, and they face formidable obstacles. We need to keep on top of our representatives, people. The ignorance in this country runs thick, but we all need to step up to the plate. Let’s show a bit of backbone.

Heh, like this guy:

35 comments